Have you ever wondered what would happen to your personal assets or savings if your business ran into serious debt or faced a lawsuit? How do you protect it?

For most businesses, the answer is to form a limited liability company, establishing a clear and legal boundary between business activities and the owner’s personal finances. So that in the unfortunate event that your business fails or is taken into court, your personal assets, including your savings, car, house, and other properties, cannot be used to repay the company’s liabilities.

But, who qualifies for an LLC, and how can businesses form one? In this guide, you’ll learn the definition of limited liability company, as well as its advantages and disadvantages, and key steps to building yours.

What is a limited liability company?

A limited liability company or LLC is a common business structure in the United States. It is a separate legal entity, like that of a corporation, that protects its owners or members from personal liability for most business debts and legal claims. At the same time, it offers the flexibility in taxation and management often found in a partnership or sole proprietorship, combining all the good features of corporations and partnerships.

Limited Liability Company Characteristics

Many business owners appreciate the balance LLCs offer, as it helps protect personal assets and avoid the complex governance requirements of corporations. LLCs operate under a flexible management structure with fewer formalities. As such, they are not required to hold annual meetings or maintain a board of directors.

Instead of corporate bylaws, LLCs are governed by an LLC Operating Agreement, which outlines ownership, management, and operational rules. This makes them suitable for small businesses, startups, and independent professionals seeking limited liability protection with minimal administrative burden.

But one of the most valuable limited liability company characteristics, business-wise, is that it gives members greater freedom in profit distribution, allowing them to determine how revenue is allocated.

Limited Liability Company vs. Partnership

While there is a lot of overlap in how both are managed and taxed, LLCs and partnerships are two separate business structures. In a general partnership, partners may not be taxed at an entity level, but they remain responsible for the business’s liabilities, which can put personal assets at risk. Additionally, in many jurisdictions, a general partnership may dissolve automatically when a partner withdraws, unless otherwise agreed.

LLC members, on the other hand, are generally protected from personal liability beyond their investment in the company. Moreover, an LLC typically continues to exist even if a member leaves, though this depends on the terms of the Operating Agreement. If the Operating Agreement addresses member withdrawal, those terms will control. If it is silent, the applicable state’s default LLC statutes will govern the process. Unlike partnerships, LLC statutes in most states provide continuity of existence despite changes in membership.

9 Types of Limited Liability Companies (with Examples)

All LLCs follow the same structure, but there are several variations depending on ownership, taxation, and purpose. Here are the nine types of LLCs to consider with specific limited liability company examples:

Single-Member LLC

A single-member LLC is owned and run by just one person or business, as the name suggests. It is popular among freelancers and solo entrepreneurs for its simplicity and liability protection. For tax purposes, the Internal Revenue Service (IRS) typically treats single-member LLCs as “disregarded entities,” meaning income and losses pass through directly to the owner’s personal tax return — no separate corporate filing needed. Thus, avoiding corporate-level taxation.

Example: Many Amazon and Etsy sellers run their businesses as single-member LLCs.

Multi-Member LLC

A multi-member LLC has two or more owners, called members. It works well for partnerships or co-owned businesses that want flexibility without the formalities of a corporation. By default, the IRS taxes multi-member LLCs as partnerships, meaning profits and losses pass through to members. However, members can elect corporate taxation if it offers strategic benefits.

Example: Typically, smaller firms in professional services like accounting and consulting use multi-member LLC structures to combine expertise and share profits.

Member-Managed LLC

In an LLC that is managed by its members, all of the owners are involved in running the business. Unless the operating agreement says otherwise, this is the default structure in most states.

This type is best for small groups where everyone wants to be involved in making decisions. It makes management easy and allows everyone to work together, but it might not be as effective as the company expands. In those cases, many businesses evolve into a multi-member LLC, where multiple owners share control and may start dividing roles to keep things organized.

Example: Startup companies such as Y Combinator Management, LLC, the LLC behind the well-known accelerator that helped launch Airbnb and DoorDash, often begin as member-managed LLCs where the founders are active owners participating directly in management and decisions.

Manager-Managed LLC

An LLC with a manager hires one or more managers, who may or may not be members, to run the business on a daily basis. Some members act more like investors and don’t take part in day-to-day management. Many bigger LLCs or businesses with passive investors use this structure. It makes roles clearer and can make scaling easier, especially when you need to centralize operational control.

Example: Companies like Cascade Investment, LLC, the private investment firm that manages much of Bill Gates’ wealth, operate with professional managers handling investment decisions while ownership remains separate.

Series LLC

A series LLC allows a parent LLC to create separate divisions, or “series,” each with its own assets, liabilities, and members. Each series operates somewhat independently under one umbrella entity.

This structure is commonly used in real estate or investment businesses that manage multiple assets. However, some states do not recognize series LLCs as domestic entities, including California and Georgia. Pushing through the formation of series LLCs in these areas might require complex interstate legal treatment.

Example: Lettuce Entertain You Enterprises, a well-known restaurant group based in Chicago, uses structured LLC arrangements to operate multiple restaurant concepts under one umbrella while keeping liabilities separated across locations.

Professional LLC (PLLC)

A professional LLC is for licensed professionals like doctors, lawyers, accountants, and architects. Some states require certain types of businesses to set up a PLLC instead of a regular LLC. It still protects members from liability, but it usually doesn’t protect them from malpractice claims related to their own professional services.

Note that different states and licensing boards have varying requirements and eligibility rules, so it’s advisable to research the area first before setting up one.

Example: Law firms like Morgan & Morgan operate as professional LLCs (PLLCs) in most states, allowing licensed attorneys to work under one entity while meeting state regulations for professional liability and licensing.

Low-Profit LLC (L3C)

A low-profit limited liability company (L3C) combines aspects of nonprofits and regular LLCs and is typically set up for businesses that want to advance their causes and help people rather than maximize profits. Tennessee, North Dakota, and Delaware are just three of the states that explicitly allow this type of LLC. States that do not recognize L3Cs cannot automatically receive tax-exempt status as nonprofits do.

Example: SEEDR L3C is an Atlanta-based, mission-driven, low-profit LLC focused on health and development solutions that has partnered with groups like the CDC and the Gates Foundation.

Anonymous LLC

An anonymous LLC is structured to keep the owners’ identities private in public records. This type is often used by investors or individuals seeking confidentiality, though anonymity may still be limited by federal reporting requirements, banking regulations, or legal disclosures. States like Wyoming, New Mexico, and Delaware are known for offering stronger privacy protections.

Example: One popular example is the Wyoming-based firm Registered Agents, Inc., which forms LLCs and acts as a registered agent, helping businesses structure ownership privately by listing its address on public filings instead of the owners’ identities.

LLC Taxed as an S Corporation or C Corporation

Although not technically different legal entities, LLCs can elect to be taxed as an S corporation or a C corporation with the IRS. This allows business owners to optimize their tax position without changing their legal structure.

Some businesses may pay less in self-employment taxes if they choose to be an S corporation, while C corporations may be better for businesses that want to reinvest or get outside investment. These elections require careful planning with a tax professional.

Example: Amazon LLC operates as a subsidiary under Amazon.com, Inc., showing how large businesses can use LLC legal structures while still being taxed as corporations within a broader corporate framework.

What are the advantages of limited liability companies?

Listed below are four reasons that have led to their widespread use in the U.S.:

Limited Liability Protection

Probably the major advantage of an LLC is the protection of personal assets. As a separate legal entity, the LLC shields its members from personal responsibility for business debts and lawsuits. This separation is especially valuable in industries with higher financial or legal risks like e-commerce and other digital services.

Pass-Through Taxation

By default, LLC profits are taxed as a sole proprietorship and reported on members’ personal tax returns, instead of at an entity level. However, it can also be taxed as a partnership or S corporation, depending on what the owner wants or what saves them the most money.

Operational Flexibility

LLCs are not subject to the formal requirements that apply to corporations, such as structured boards and detailed governance processes. As such, it makes LLCs easier to manage, particularly for small teams or owner-operated businesses.

Flexible Ownership Structure

LLCs can be established by a single individual or multiple members, including other companies. Having this versatility in the organization supports a wide range of business models, from solo ventures to joint enterprises.

What are the disadvantages of limited liability companies?

Despite the benefits, LLCs also have drawbacks that are worth looking at before pursuing this business structure:

Self-Employment Taxes

Members are often required to pay self-employment taxes and fees on their share of profits, which can increase overall tax obligations depending on income and tax elections.

State-by-State Regulations

Regulatory requirements for LLCs vary by state, including formation fees and reporting obligations. This variability can add complexity, especially for businesses operating in multiple states. Some states in the U.S. charge franchise fees to business entities regardless of income or current standing. For instance, in California, they impose a minimum tax of $800 to be paid annually.

Capital Raising Limitations

LLCs may face challenges in raising capital because they cannot issue stock. This limitation can make it more difficult to attract venture capital or institutional investors compared to traditional corporations. That is why companies planning rapid expansion or public offerings often select corporate structures instead.

Ownership Transition Complexity

As convenient as it is to have flexibility in management and control, transferring ownership may be a bit of a challenge. Adding or removing members may require changes to operating agreements and formal legal documentation, which can create administrative challenges as the business expands.

How to Start a Limited Liability Company

Forming an LLC in the U.S. is relatively straightforward, but the exact steps can vary depending on the state. While requirements differ slightly, most entrepreneurs follow a similar process:

1. Choose a U.S. State for Formation

Before registering your LLC, you need to decide where to form it. In most cases, the best choice is the state where you live and actively operate your business. Forming an LLC in another state may seem attractive, but it often requires registering as a foreign LLC in your home state — which can mean additional costs and administrative work.

Business-friendly states like Delaware, Wyoming, and Nevada are popular due to their tax policies and flexible business laws. However, forming in these states typically makes sense only if your business has no physical presence in another state, such as an online-only operation or one run by a non-U.S. resident.

2. Name the Business

Most states require the name to include “LLC” or “Limited Liability Company” and prohibit certain restricted terms, such as “Bank” or “Insurance,” unless approved. If you already have a preferred name, many states allow you to reserve it temporarily (60-120 days) for a small fee while preparing your formation documents.

3. File Articles of Organization

The next step is to file Articles of Organization, or Certificate of Formation in some states, with the relevant state agency. This document formally establishes the LLC and includes information such as the business name, address, and registered agent.

Many states allow online filing, with processing times ranging from same-day approval to several weeks, depending on the jurisdiction. For example, certification in Illinois may take up to 10 business days, while states like Wyoming can offer same-day processing.

4. Create an Operating Agreement

Businesses often create an operating agreement to define ownership structure, roles, responsibilities, and profit-sharing arrangements. Although not always legally required, this document provides clarity and helps prevent disputes among members.

5. Obtain an EIN

After formation, most LLCs obtain an Employer Identification Number (EIN) from the IRS. The EIN is required for filing federal taxes, hiring employees, and opening business bank accounts. Applying for an EIN is free and can usually be completed online in minutes through the IRS website. Once approved, the number is issued immediately and can be used for federal compliance and financial operations.

Frequently Asked Questions

Does a limited liability company have a board of directors?

LLCs are not required to have a board of directors. Unlike corporations, LLCs offer flexible governance structures and can be managed directly by members or by appointed managers.

How do LLC owners make money?

LLC owners earn income primarily through profit distributions. Since most LLCs use pass-through taxation, profits are reported on members’ personal tax returns. In some cases, members may also receive salaries or structured payments, depending on the LLC’s tax election and organizational structure.

Is an LLC good or bad?

An LLC is not inherently good or bad. Its suitability depends on the business’s goals and growth plans. It is often ideal for small businesses, freelancers, and closely held companies seeking liability protection without extensive compliance requirements. Businesses seeking venture capital funding or planning to go public may prefer corporate structures.

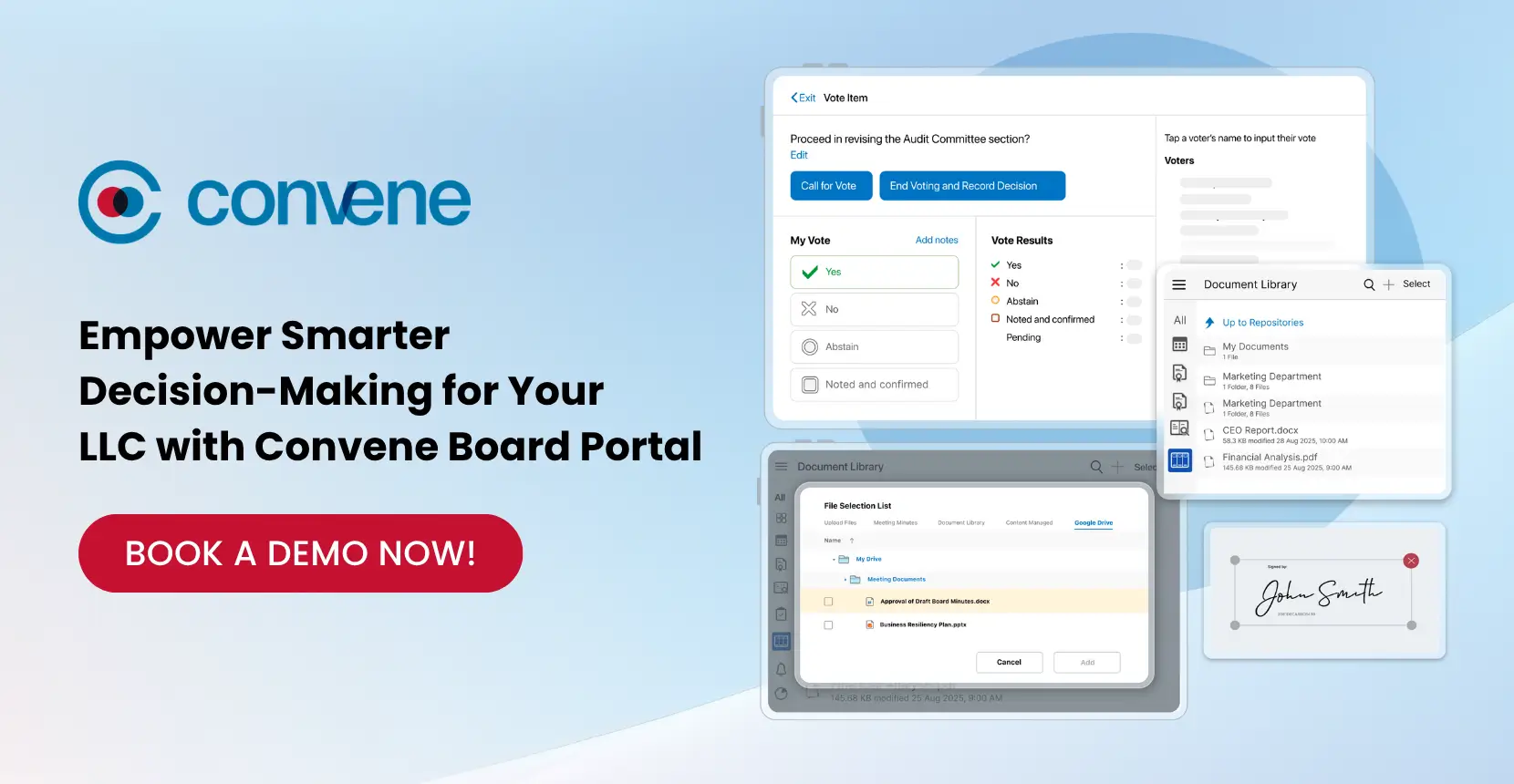

Empower Smarter Decision-Making for Your LLC with Convene Board Portal

By separating personal assets from business liabilities and maintaining adaptable management and tax structures, LLCs have become one of the most widely used business entities in the U.S. Along with this growth, their governance needs to evolve. Managing internal documents, coordinating decisions among members, ensuring compliance, and maintaining transparency can become increasingly complex, particularly for multi-member LLCs or organizations expanding operations.

Digital governance solutions such as Convene Board Portal can help address these challenges.

As one of the leading board management and governance tools in the U.S., Convene allows LLCs to store critical documents in one centralized location and streamline communication and decision-making among stakeholders through Review Rooms and Resolutions. Features like secure document sharing, role-based access controls, real-time collaboration, and compliance-ready recordkeeping enable LLCs to operate with the structure and professionalism of larger enterprises.

Request a demo today and discover how Convene can support your organization’s growth with modern, secure governance built for the future.

Jess is a Content Marketing Writer at Convene who commits herself to creating relevant, easy-to-digest, and SEO-friendly content. Before writing articles on governance and board management, she worked as a creative copywriter for a paint company, where she developed a keen eye for detail and a passion for making complex information accessible and enjoyable for readers. In her free time, she’s absorbed in the most random things. Her recent obsession is watching gardening videos for hours and dreaming of someday having her own kitchen garden.

- Connect:

-