Capital is a prerequisite when starting a business. Entrepreneurs need funds to complete business registrations, secure licenses, purchase equipment, and hire employees. Without sufficient funding, it will be challenging for new businesses to operate and scale efficiently.

One way to secure funds is through start up business loans. This method has helped entrepreneurs build startup companies from the ground up. In the United States, census data shows that the Small Business Administration (SBA) supported 103,000 small business financings in 2024, the highest level across loan programs since 2008. For U.S. startups, the external financing has alleviated the pressure on founders to draw on their personal funds for growing the businesses.

Explore how start up business loans empower entrepreneurs to pursue their business visions. Discover their benefits, requirements, examples, and best practices for choosing a lender.

What is a startup business loan?

Entrepreneurs use start up business loans to start a new business — providing capital for ventures such as leasing an office space, hiring a board of directors and staff, and buying equipment.

The latest survey by the Academy Bank in 2025 discovered that 65.8% of small business owners have reported using financing at some point in their operations. This suggests that borrowing money is a common strategy among small business entrepreneurs.

How much do startups borrow? According to the same survey, 69.9% of respondents borrowed up to 100,000 USD, just enough to solve specific operational problems or target immediate opportunities.

There are multiple ways for entrepreneurs to obtain start up business loans. They could apply for government loan programs, private financing companies, or nonprofits. Unlike traditional bank loans, business loans for startups offer more flexible repayment terms and lower interest rates, which are ideal for starting businesses. Since business startups lack operating or revenue history, lenders would require founders to present their personal credit score, business plan, and financial projections.

How can startup business loans support long-term growth?

Personal savings can help run the initial phases of startups, but eventually, the board of directors will need additional funds to invest in growth opportunities. Here are the top reasons why businesses apply for a startup loan:

1. Facilitate business expansions

Startups seek loans to support their expansions. Instead of waiting for profits or relying on initial capital, loans provide immediate access to funds without compromising cash flow or daily operations. However, leaders should only apply after thorough market research and financial statement analysis to assess potential risks and returns.

2. Strengthen inventory management

Product-centered businesses can leverage quick business loans to increase purchasing power and expand inventory. By buying in bulk, they can lower costs and improve profit margins, which is a critical advantage in fast-moving industries like retail, fashion, food and beverages, and pharmaceuticals.

3. Invest in essential equipment

The startup business loan can ease the financial weight of investing in equipment upfront. Businesses won’t have to wait for revenue to acquire specialized tools, technology, or vehicles. They can use the fund to invest in the necessary assets and repay the loan as revenue grows.

4. Hire high-skilled talent

Hiring specialized professionals involves money. The startup business loan may be spent on employee recruitment, training, and salaries — even before revenue. This allows businesses to hire high-skilled employees as soon as they start operations, ensuring quality service to clients.

5. Support product development

Designing and prototyping new products can be costly, depending on the product. Businesses may seek business loans for startups to fund the research and development process, gaining them additional resources for purchasing materials or facilities.

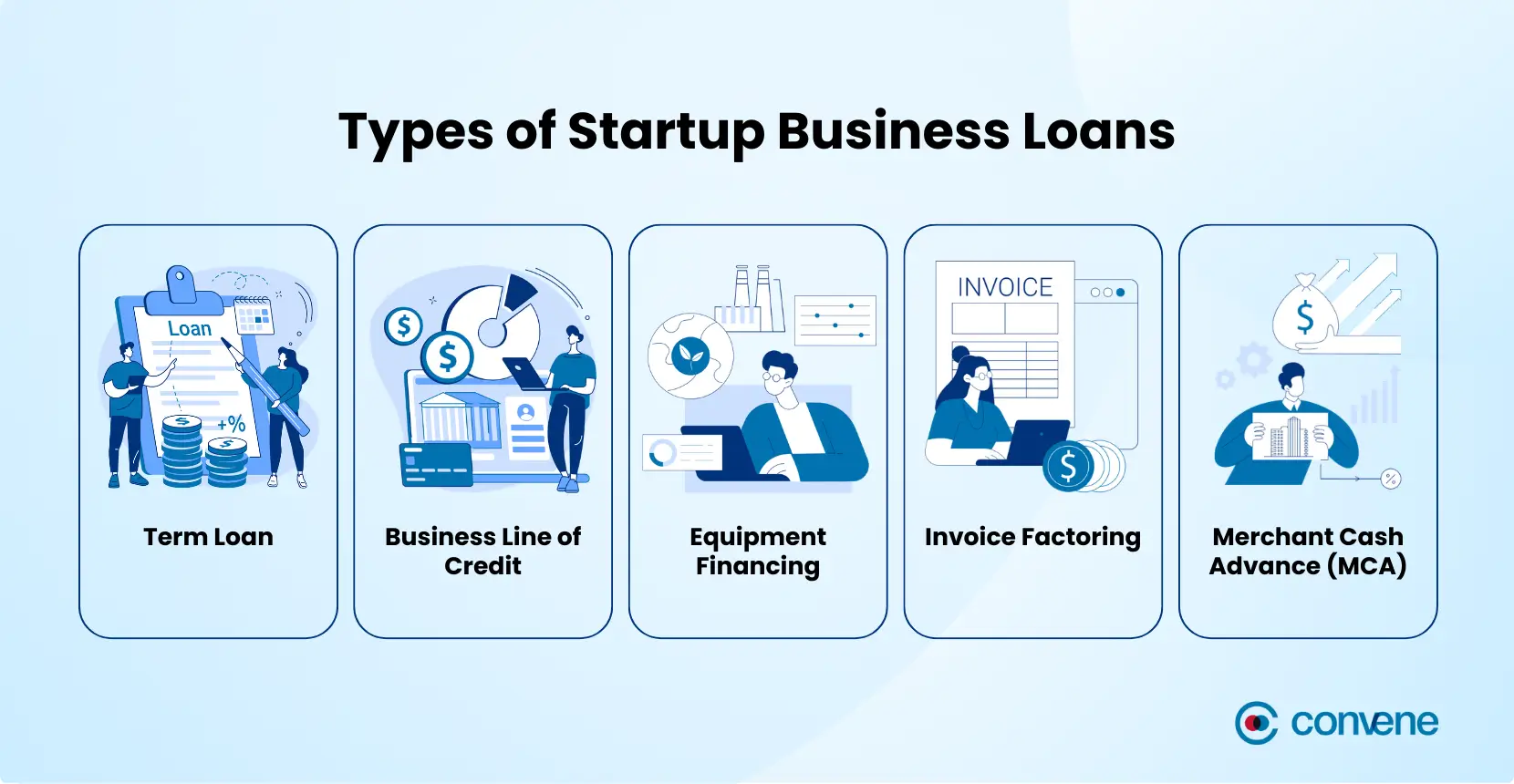

Types of Startup Business Loans and Examples

Startups can choose from a wide selection of small business loans, including:

Term Loan

A term loan refers to a lump sum of money that borrowers must repay over a fixed period, usually with interest. Term loans are categorized based on their repayment duration:

- Short-term loan: Loans that run less than a year or up to 18 months are considered short-term loans. They are generally for startups that don’t yet have an established credit history.

- Intermediate-term loan: This lasts between one and three years, commonly with monthly repayment terms.

- Long-term loan: This can last up to 25 years and would often require businesses to present collateral.

OnDeck is a financial company that specializes in fast financing for startups. It offers loans ranging from 5000 to 400,000 USD, with repayment terms of up to 24 months. This makes the company suitable for those seeking short-term or intermediate-term business loans for startups.

Business Line of Credit

This is comparable to a credit card, where businesses can draw funds up to a certain limit. Unlike a term loan, its payment timeline is not fixed, and borrowers may only pay the accrued interest monthly.

Requesting funds through this method is relatively faster than other financing options, making it ideal for resolving cash flow gaps. Additionally, they are widely offered by banks or online platforms.

One example is Fundible. Recognized by Forbes as one of the best business lines of credit for startups, this lending company offers same-day approval and funding. It’s a practical option for businesses seeking immediate access to additional capital.

Equipment Financing

Businesses apply for equipment financing to acquire assets without making large upfront payments. These may be furniture, computers, machines, medical tools, company vehicles, or specialized software like board portal software.

There are two options for equipment financing:

- Loan to purchase equipment: The borrowed money is allocated for purchasing equipment. Equipment shall serve as collateral for the loan, granting lenders authority to repossess if the borrower fails to repay the loan.

- Equipment leasing: Under this option, businesses use the equipment through monthly rental fees instead of purchasing. This avoids repeated large investments and can upgrade equipment faster with fewer liabilities.

The U.S. Business Funding Equipment Financing earned the top spot in Forbes’ Best Equipment Financing for 2025. Unlike many lenders that require at least two years of time-in-business, U.S. Business Funding Equipment Funding offers financing even to those who have just started operating for as short as six months.

Invoice Factoring

This is a short-term funding option where businesses convert their accounts receivable into immediate cash. Large clients often take between 30 and 90 days to pay, which slows down cash flow for businesses. Instead of waiting for the payment, businesses can sell their invoices to a factoring company based on the value of the outstanding receivables, preventing operational disruptions.

FundThrough is a leading provider of invoice factoring in the U.S. market. Its AI-powered platform enables faster approval and funding compared to traditional banking. This makes their product convenient for businesses seeking urgent access to working capital.

Merchant Cash Advance (MCA)

MCA is a lump sum in exchange for a percentage of future daily sales. Unlike traditional banking loans, repayment for MCA can be made through daily or weekly sales deductions and uses a factor rate instead of interest.

This is one of the most accessible funding sources for startups, particularly for those with steady sales but limited credit history. According to the 2024 Small Business Credit Survey by the Fed’s Findings, 58% of applicants were granted this funding compared to 30% for business loans startups.

An example is Credibly, which stands out for its flexible requirements. With only government-issued ID, bank statements, and signed receivables or purchase agreements, businesses can be granted funding in as fast as 24 hours.

Where to get start up business loans?

There are several key sources from which startups can obtain funding, depending on their credit profile, time-in-business, and objectives.

- Traditional Banks: These are best suited for startups with a more stable revenue and experienced founders because they offer competitive rates. Since they are traditional, they typically require strong credit, extensive financial documentation, and collateral.

- Online Lenders: Startups have a higher chance of approval with these financing companies because they have a more straightforward application process. However, in turn, they have higher interest rates.

- Government-Backed Programs: National and local governments collaborate with established financial institutions to offer start up business loans with lower interest rates and longer repayment terms. The Small Business Administration in the US. partially guarantees the loans, aiding repayments if the business is unable to do so. This reduces risk for lenders, encouraging them to lend more.

- Private Equity Firms: Although not loans, angel investors or venture capital extend equity funding to high-potential startups or small businesses in exchange for ownership. This is ideal for those who prefer not to take on debt.

Startup Business Loan vs. Small Business Grant: Key Differences Entrepreneurs Should Know

What makes a startup business loan different from a small business grant? Choosing the right funding option impacts long-term success.

Understand the differences to help you identify which option fits your business more.

To help you grasp how the King Code has evolved, the table below highlights the key shifts from King IV to King V.

| Small Business Grant | Startup Business Loan | |

|---|---|---|

| Source | Governments and nonprofit organizations typically offer this grant without repayment terms. (Examples: Small Business Administration (SBA) and the U.S Department of Agriculture (USDA)) | Banks, private lenders, or investors approve capital to businesses with interest and definite payment terms. (Examples: OnDeck, Fundible, FundThrough, and Credibly) |

| Interest Charges | No interest | Interest depends on the payment timeline and loan amount |

| Eligibility | Requires applicants to submit comprehensive proposals because selection is competitive | Lenders approve loan requests based on revenue data, cash flow, collateral, and credit score |

| Approval Time | May take weeks to several months | May take hours, weeks, or month, depending on the lender’s processing time |

| Usability | Must be strictly used for the proposed purpose | Flexible use |

| Funding Amount | Often within a set amount | Can range from small to large amounts, depending on eligibility |

What are the requirements when applying for a startup business loan?

Applying for a business loan as a startup can be challenging due to the lack of credit and revenue history. However, there are other factors that lenders consider, such as:

Owner’s Credit History

Since startups don’t have an established credit history yet, lenders rely on the owner’s credit score for risk assessment. Most lenders prefer a credit score of 690 and above, as this reflects repayment discipline and financial stability.

Additionally, lenders also assess the capability to repay through the debt service coverage ratio, which divides net profit by annual debt amount. Startups whose owners have strong credit histories and healthy debt ratios are more likely to be approved for higher funding and better interest rates.

Robust Business Plan

Submitting a comprehensive business plan shows how operations flow and how revenue will be made. Lenders must understand the business’s strategy for profitability and sustainability. An effective business plan includes an executive summary, operational plan, and financial forecasts.

Applying for a business loan involves collaboration between the owners, finance teams, and advisors. Conducting meetings in a centralized and secure platform like board portals helps keep financial documents, board approvals, and business plans aligned. This ensures all stakeholders are on the same page during the funding process.

Collateral

It’s common for lenders to require collateral or personal guarantees for loans for start up. Since the business has little to no assets yet, owners may front their personal possessions as security. This reduces risks for lenders and may improve chances of loan approval.

Legal Documentation

Lenders need to legitimize a business by reviewing its legal documents. This requires businesses to submit their business licenses, registrations, and relevant permits.

As startups scale, it becomes harder for the management to organize corporate records. Storing legal documents in digital board portals ensures authorized people have quick access to requirements, enabling faster processes.

Industry Experience

Lenders view startups as high-risk ventures due to their weak financial track record. To measure the likelihood of repayment, they would assess the board’s competencies and governance performance.

Best Practices When Applying for a Startup Business Loan

Applying for a startup loan is more than simply selecting a lender. Management should establish a clear strategy to improve the chances of approval and avoid costly mistakes.

Follow these best practices to stay organized and reduce risks when applying for startup business loans.

- Determine loan type: Identify the type of loan your business will pursue based on financial and overall business goals and repayment capacities.

- Compute hidden fees: Double-check processing fees for unstated charges apart from the usual service and administrative charges.

- Evaluate repayment terms: Review the repayment schedule, as well as guidelines/penalties for late payments.

- Compare requirements: Understand the requirements of each lender and determine which one you’re most eligible for.

- Ask for approval timeline: Plot approval times to ensure you choose one that aligns with your strategy.

- Review reputation and customer support: Conduct due diligence on the credibility of lenders by checking online reviews, ratings, testimonials, and even complaints. Moreover, identify how responsive and knowledgeable the support teams are. Choose a lender that has a smooth process and helps resolve issues promptly.

- Document board-level decisions: Before finalizing any decision, ensure that loan applications, repayment commitments, and risk assessments are carefully documented and stored. Putting this information in a secure board portal maintains transparency and accountability among management.

Frequently Asked Questions on Startup Business Loan

Is it possible to secure a startup business loan without revenue?

Yes. It’s possible to get a startup business loan without revenue history, however, expect that it will be more challenging. Since lenders typically approve applicants with existing records, businesses need to provide additional proof to build their credibility. In these cases, a detailed business plan and personal collateral are often required.

How much can a startup get from a business loan?

The amount depends on the time-in-business, but generally, startups or small businesses secure between 5,000 and 5 million USD. However, for startups that are in their early stages, they can usually obtain up to 250,000 USD only until they have a strong credit and proven revenue history.

Additionally, since startups are high-risk, lenders typically charge higher interest rates compared to established businesses. Bank loan rates are between 5% and 16%. SBA loans’ annual percentage rates are up to 6.5%, while online lenders can charge as high as 75%.

Streamline Financial Decisions and Enhance Funding Readiness with Convene Board Portal

Securing loans for start ups requires more than just financial statements. It involves a structured cycle of board meetings, approvals, risk assessments, and compliance tracking. It’s critical to understand that lenders and investors not only assess financial health but also governance effectiveness.

Convene Board Portal supports startups by providing a centralized hub for these governance processes. Leaders can collaborate with peace of mind, knowing that their resolutions, financial analysis, and action items will be stored securely within a controlled environment.

Instead of relying on email threads and shared drives, leaders can:

- Consolidate confidential legal and financial documents, such as cash flow reports, loan agreements, and court filings, in a single space.

- Digitize the approval process related to funding commitments and loan applications.

- Control access permissions across the organization to protect sensitive financial and management information.

- Automate note-taking and file retrieval using Convene AI.

- Track every action using audit trails and detailed document versioning.

Book a Convene Board Portal demo and discover how it empowers leaders to enhance organization and strengthen governance practices.

Jean is a Content Marketing Specialist at Convene, with over four years of experience driving brand authority and influence growth through effective B2B content strategies. Eager to deliver impactful results, Jean is a data-driven marketer who combines creativity with analytics. In her downtime, Jean relaxes by watching documentaries and mystery thrillers.

- Connect:

-

-